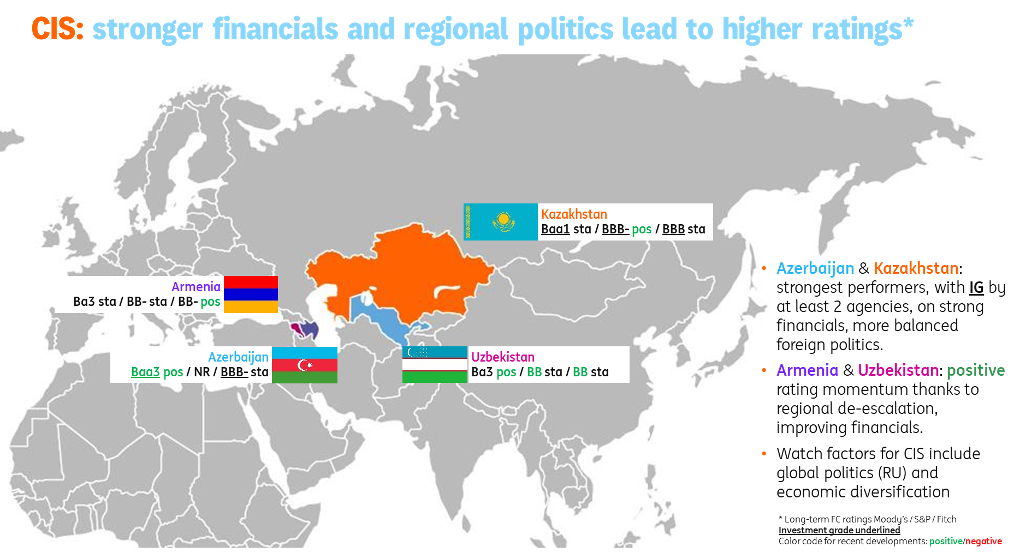

Reading CIS Economies in an Era of Uncertainty

Global trade tensions rarely hit CIS economies head-on. More often, they work their way through a handful of familiar mechanisms—above all through commodity prices and demand from key trading partners. Once those mechanisms are broken down, it becomes much easier to assess macroeconomic resilience and understand where risks are most likely to emerge: in the budget, the current account, inflation, or the exchange rate.

Dmitry Dolgin, Chief Economist for Russia and the CIS at ING Bank N.V., shared his framework for analyzing four economies in the region: Armenia, Azerbaijan, Kazakhstan, and Uzbekistan. The logic of the exercise is straightforward: first, identify which external transmission channels matter most for a given economy; then assess which domestic factors amplify or soften their impact.

Three Channels of External Shock Transmission

Within the CIS space, the focus here is on four countries: Armenia, Azerbaijan, Kazakhstan, and Uzbekistan. The channels themselves are broadly the same, but their weight varies significantly from one country to another.

1. Oil: impact on exports and the budget

(primarily Kazakhstan and Azerbaijan)

The first channel is the oil price. In 2025, oil remained under pressure, partly due to US policy, which supported domestic oil production and pushed OPEC to compete more on volumes than on price. For the economies in question, this matters because oil prices directly shape export receipts and public finances.

Kazakhstan and Azerbaijan are by far the most exposed, given the large share of export revenues generated by the oil sector. In 2025, oil and gas accounted for around 53% of Kazakhstan’s export proceeds and roughly 86% of Azerbaijan’s exports. From a fiscal perspective, the sector contributed about 15% of consolidated budget revenues in Kazakhstan and 50% in Azerbaijan.

In terms of annual average oil prices, each additional dollar per barrel brings Kazakhstan roughly $580 million in export revenues and around $150 million in budget revenues. For Azerbaijan, the comparable figures are about $300 million and $210 million, respectively. That is why any revision in the oil outlook quickly feeds into current-account and fiscal projections.

Azerbaijan is more sensitive to oil price swings, but also more financially resilient thanks to larger reserve buffers, which give the country more room to absorb adverse volatility.

2. Gold: a positive external impulse in times of uncertainty

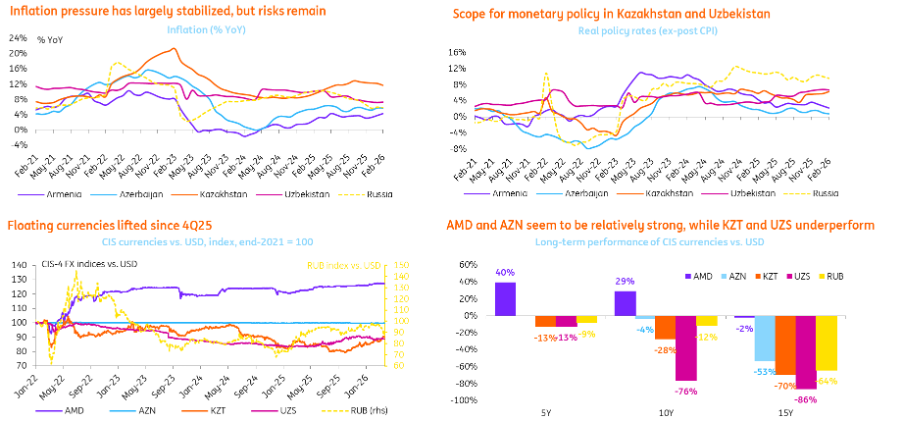

The second channel is the gold price. Gold tends to rise in periods of uncertainty, which creates a positive external impulse for producer countries. In 2025, the gold price climbed from $2,500 to around $4,500 per ounce.

For Uzbekistan, this is critical. Every additional $1,000 per ounce generates roughly $4 billion in annual export revenues. If gold remains near $4,000, annual export proceeds from gold could rise sharply—from $7.5 billion in 2024 to $15 billion in 2026, effectively doubling over two years.

This channel is important not only because of its export effect, but also because it feeds directly into exchange-rate dynamics: higher gold prices can support the domestic currency by strengthening the balance of payments.

3. Secondary effects via trading partners: the second-round channel

The third channel is indirect spillovers via trading partners. In 2025, US trade policy was directed primarily at the EU and China, raising concerns about slower GDP growth in both.

The EU and China together account for 50–60% of external trade for the countries under review. This means that aggressive US actions that slow growth in Europe and China can generate second-round effects for CIS economies as well. Armenia stands out here in a positive sense: it is far less dependent on trade with the EU and China, which together account for only around 10–20% of its trade turnover.

Country-specific domestic fault lines: where the pressure shows up

Armenia: growth remains strong, but momentum is fading; the currency looks overvalued

Armenia is the smallest economy among the four, yet it has posted strong growth rates. Still, its medium-term growth outlook is becoming less favorable. One reason is the slowdown in the inflow of highly skilled migrants from neighboring countries—a major growth impulse in 2022 that is now gradually fading.

Another source of uncertainty is the exchange rate. The dram remains exceptionally strong, raising the question of whether it can continue to be supported by remittances and capital inflows. Overall, this leaves Armenia relatively vulnerable to both global and regional shocks.

Azerbaijan: financially resilient, but the current account is highly sensitive to oil prices

Azerbaijan appears to be the most financially resilient of the four economies. But the domestic fault line here lies in the fact that physical output growth in the oil sector is slowing as fields mature. The gas sector, despite new contracts, is not yet in a position to fully offset any decline in oil production.

The second major issue is the balance of payments: the current-account surplus has been narrowing in recent years, including through late 2025. At the same time, the exchange rate remains pegged to the dollar at 1 USD = 1.7 manat. The key long-term question, therefore, is how sustainable that peg really is. If oil were to fall sustainably below $60 per barrel, the risk of a current-account deficit and pressure on the currency would rise materially.

Kazakhstan: fiscal consolidation, inflation, and the state’s role in the FX market

For Kazakhstan, the key issue is the impact of fiscal consolidation over the next few years. A VAT increase from 2026 could improve the fiscal position, but it also creates inflation risks. In 2025, there was already a partial front-loading of price adjustments ahead of the tax change, which in turn required a policy rate hike to 18.00%.

Kazakhstan’s FX market is heavily influenced by fiscal policy. The larger the budget deficit, the higher the drawdowns from the sovereign fund—and those drawdowns require FX sales in the domestic market. In that sense, a wider deficit can actually be supportive of the exchange rate. If the government follows through on its commitment to reduce the fiscal deficit and cut sovereign fund spending, then FX stability will increasingly depend on whether other positive forces—such as capital inflows or an improved current account—step in to compensate.

Uzbekistan: fiscal consolidation, inflation control, and gold support for the currency

Fiscal consolidation is also central in Uzbekistan. The country has delivered a fairly aggressive reduction in its budget deficit, which had previously been a source of concern, so the recent trend can be seen as encouraging. A second positive factor is inflation, which appears to be under control despite the liberalization of household utility tariffs.

The third element is directly linked to the global backdrop: high gold prices have noticeably improved the currency’s performance. Over the past 15 years, the Uzbek sum had been the weakest currency among the four, but since 2025 it has shown some recovery. The question is how long that recovery can continue—and how dependent it is on favorable external pricing.

This article has been updated in light of developments in the Middle East.

After the article was initially written, a new external shock emerged: the escalation of the conflict in the Middle East in March 2026. The transmission channels described above remain relevant, but for some countries in the region the direction of the effect has changed. Earlier, the main risk had been seen as weaker oil prices. Under the current configuration, by contrast, higher commodity prices now appear more likely.

For the region’s oil exporters—Kazakhstan and Azerbaijan—this implies a short-term improvement in external metrics. According to ING estimates, a sustained $10-per-barrel increase in oil prices could add around $6 billion to Kazakhstan’s annual exports and $3 billion to Azerbaijan’s exports—roughly 1.8% and 4.0% of GDP, respectively. The fiscal effect is also positive: such a move in oil prices could generate around $1.5 billion in additional budget oil revenues in each country.

Uzbekistan benefits through a different commodity channel: gold. A $1,000 increase in the gold price per ounce could generate around $4 billion in annual export revenues, equivalent to roughly 2.7% of GDP.

At the same time, another transmission mechanism becomes stronger: imported inflation. Despite limited direct trade between the countries in question and the immediate parties to the conflict, dependence on broader supply chains—through the EU, Turkey, the Gulf states, and Iran—means that rising commodity prices and potential logistics disruptions could add to inflationary pressure.

As a result, the balance of effects differs across the region:

- Armenia appears the most vulnerable, given its dependence on imported energy and its geographic proximity to the conflict zone;

- Azerbaijan also borders Iran, but benefits from higher commodity prices;

- Kazakhstan gains support via oil, but remains exposed to volatility in global financial flows;

- Uzbekistan appears the most resilient, thanks to gold exports.

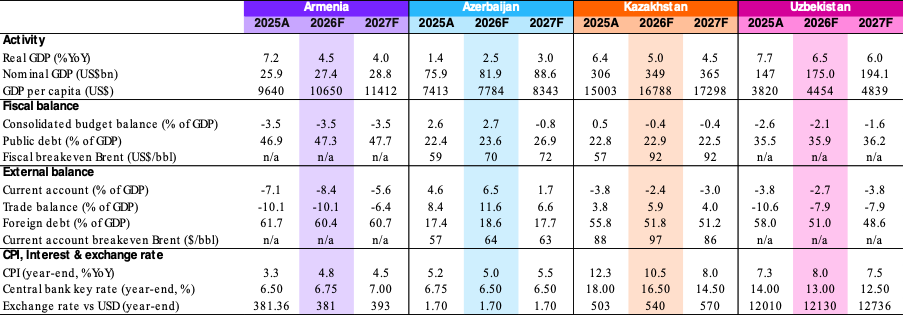

Inflation, rates, and exchange rates across the main CIS economies

Key indicators: 2025 actuals and ING forecasts for 2026–27

Practical takeaways: what matters in practice

- For Kazakhstan and Azerbaijan, oil remains a source of financial support through both export revenues and fiscal receipts. Any shift in the oil scenario—whether toward lower or higher prices—first shows up in the current account and public finances.

- For Uzbekistan, gold is currently the key external support factor. It can improve balance-of-payments metrics and support the currency, although much also depends on fiscal discipline and inflation control.

- Trading partners matter as carriers of second-round effects. Slower growth or rising inflation in the EU, China, Turkey, and the Middle East should also be monitored as indirect external shocks that are effectively imported into CIS economies through the trade channel.

- Domestic macro policy matters no less than the external backdrop. Fiscal consolidation, FX-market conditions, and inflation dynamics determine the extent to which a country can cushion an external shock—especially in an environment where imported inflation may rise through commodity prices and trade-link disruptions.

If one looks at the region merely as a collection of individual countries, it is easy to get lost in headlines and scattered data points. But keeping the transmission channels in mind helps establish priorities around the key variables—and ultimately distinguish between areas where a shock can be absorbed by domestic stabilizers and areas where it can turn into a genuine problem for the budget, the current account, inflation, or the exchange rate.

The practical value of this framework is that it helps structure incoming information. Instead of trying to react blindly, it is enough to keep asking a few regular questions: which external channel is dominant right now, which domestic factors amplify or dampen its effect, and what signals might indicate that the situation is beginning to turn. In an environment where uncertainty has become the norm, that is the real competitive edge—not the boldest forecast, but a more accurate structure for observation and decision-making.

Currency Volatility and Bank Margins: How to Measure the Effect and Calibrate FTP

Exchange-rate volatility in Turkey after 2018 has become not an episodic shock but a persistent factor linked to the dynamics of banking margins. Once this relationship is measured and the influence of local and global factors is separated, it becomes a practical tool. The estimated sensitivity of margins to volatility can then be used as a reference parameter for Funds Transfer Pricing (FTP).

Customer Centricity in the Age of Automation: Where Technology Stops Serving the Need

In the age of AI and end-to-end automation, banks risk losing a less measurable but critically important source of competitive advantage — trust and the quality of client relationships. How can RFPs be used as a structured signal of future client expectations? Where should the human remain in the process? And how can co-creation be embedded into product development through the H.E.A.R.T. framework?