Turkey 2026: Economic Stability, the Lira and Key Risks for Business

Companies planning production, sourcing, exports, or investments in Turkey in 2025–2026 face a practical question: is the current normalization the beginning of a sustainable trajectory, or merely a temporary pause that could be disrupted by the next shock?

The answer affects how companies price currency risk in contracts, how far ahead they plan, when to scale operations, and when to remain cautious.

Şevin Ekinci, an expert in Turkish macroeconomics and financial markets, suggests looking at 2026 as the year that will reveal whether the current normalization can truly hold. In this article, she explains which domestic indicators matter most, how the global environment is changing — from growth and interest rates to trade routes — and which risks could quickly reverse the current trajectory.

2026 as a Test of Sustainability

I suggest viewing 2026 as a test: will the current normalization become entrenched, or will it collapse under the first serious pressure? To understand this, it is useful to keep two things in mind: what has already been done domestically, and what conditions will shape the global environment around Turkey.

First, it is worth looking at how the economy and politics inside the country have evolved. Then we can examine the external environment and why it matters for Turkey.

One important detail specific to Turkey: I consider the exchange rate to be a central element of the economy. Every country has its own sensitive indicators. For the United States, these might include unemployment or GDP growth. For Turkey, however, the exchange rate has historically been the key barometer.

That is why the stability of the lira is one of the most important signals that the country is moving out of a crisis zone.

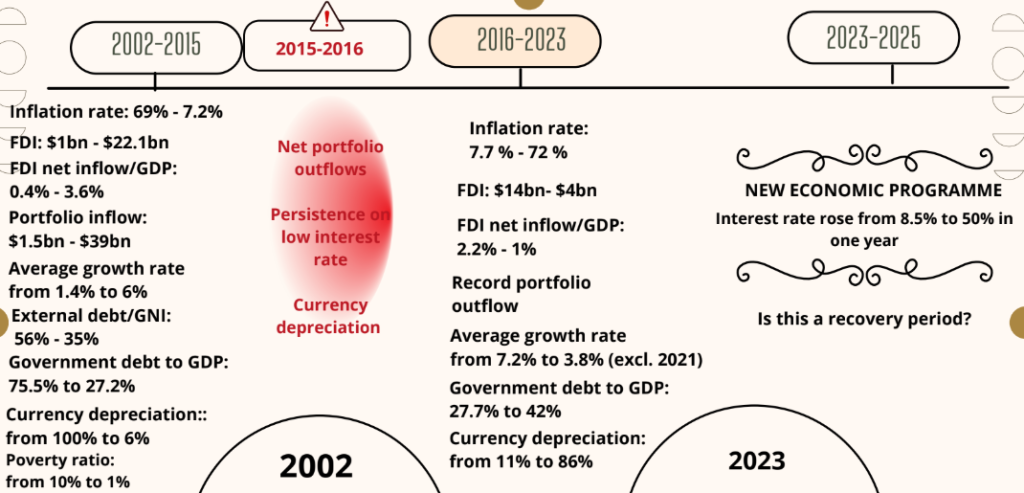

Where We Came From: Three Periods

1) 2001: Crisis and Reset

In 2001, Turkey experienced a severe financial crisis. At the time, the country operated under a fixed exchange-rate system, and the Turkish lira depreciated by roughly 100%. Inflation tripled, reaching triple-digit levels, and interest rates spiked to as high as 3000%. GDP contracted sharply.

This period demonstrated how quickly macroeconomic imbalances could spiral out of control. In response, Turkey introduced a stronger institutional framework for the financial sector.

2) 2002–2015: Reform and Recovery

After 2002, Turkey implemented major reforms and launched a program with the IMF. The economy entered a period of recovery.

According to available data:

- inflation fell from 69% to 7.2% (sometimes reaching 5–6% in individual months);

- foreign direct investment increased from $1 billion to $20–22.1 billion;

- portfolio inflows rose from $1.5 billion to $36–39 billion;

- average GDP growth reached around 6%, compared with 1.4% before 2002;

- public debt-to-GDP declined from 75.5% to 27.2%;

- currency depreciation slowed dramatically from around 100% to 6–11%;

- poverty fell from 10% to 1%.

This recovery did not happen by chance. It was built on a framework where declining inflation and currency stabilization increased predictability. And predictability is the fuel for investment, trade, and long-term planning.

3) 2016–2023: Policy Errors and Instability

A turning point came after 2015–2016. The period leading up to 2023 was marked by policy mistakes and unconventional economic policies — particularly the aggressive pursuit of low interest rates despite high inflation, contradicting fundamental macroeconomic principles.

At the same time, political uncertainty increased, further undermining investor confidence.

Key indicators during this period included:

- inflation rising to 72%;

- FDI net inflows as a share of GDP falling from 2.2% to 1%;

- record portfolio outflows of $18 billion in 2022;

- annual currency depreciation reaching 86%;

- public debt-to-GDP increasing to 42%.

Experience showed that cheap money without inflation control and policy credibility does not produce sustainable growth. Instead, high uncertainty shortens investment horizons.

Where We Are Today: Signs of Stabilization

There are indications that the government has returned to a more orthodox economic approach and formed a new economic team. One important factor supporting confidence has been the absence of political interference in monetary policy.

The current macroeconomic profile looks as follows:

- inflation: 33.3%

- GDP growth: 3.6%

- policy rate: 40.5%

- current account balance: –0.8% of GDP

- public debt: 24.7% of GDP

- Manufacturing PMI: 46.7

- unemployment: 8.5%

Reducing inflation from 80% to 33% — with a target of around 30% by year-end — can be seen as a success. However, inflation remains very high.

Stabilization has come at a cost: economic growth has slowed, but financial stability has improved. For businesses, this means that the economy is moving from a phase of major imbalances toward a phase of adjustment under tighter financial conditions.

Another important signal is the exchange rate: the annual depreciation of the lira has slowed from 86% to 18%, a significant marker of stabilization.

The Global Environment Toward 2026

The external environment also matters. Developed economies are currently entering a phase of monetary easing, with interest rates expected to decline.

The main uncertainty concerns global growth. Forecasts point to a slowdown, partly driven by trade tariffs and geopolitical fragmentation.

Current expectations for global growth are approximately:

- emerging markets: 4.2%

- global economy: 3.2%

- developed economies: 1.6%

At the same time, new risks are emerging for global manufacturing due to tariff policies. However, lower growth and lower interest rates in developed economies can also create conditions that are more favorable for emerging markets — including reduced financial pressure, potential weakening of the US dollar, and shifts in trade routes.

Opportunities for Turkey in 2026

I see several potential opportunities combining both global and domestic factors.

1) Monetary easing in developed economies

If interest rates decline in advanced economies, emerging markets typically become relatively more attractive. For Turkey, this primarily affects capital flows and financing conditions.

2) Shifts in trade routes and export potential

In recent years, global trade routes have been reorganizing. This creates opportunities for Turkey in terms of export growth and tourism revenues. Much will depend on whether companies can realize this potential and whether policy supports it.

3) Peace process and constitutional reform

Two domestic developments could also play a significant role:

- a potential peace process aimed at resolving the 45-year conflict with the PKK, which could unlock substantial economic potential;

- a new constitution, which could help create a more democratic and stable institutional environment.

4) A more cautious policy approach

The shift in policy approach may also be linked to the protests in March 2025, which signaled changing public expectations.

Under stable political conditions and favorable global dynamics, 2026 could become a year of restored confidence among international investors.

The Two Risks That Could Reverse the Trend

There are two major risks that could quickly undermine the current normalization.

The first is political risk. For Turkey, this has always been a sensitive area. If discussions about early elections intensify again, investors may hesitate to enter the market, fearing that the rules of the game could change.

The second risk is inflation inertia. Reducing inflation from 80% to 30% through high interest rates is difficult but manageable. Bringing inflation down from 30% to single digits, however, is far more challenging. Achieving that requires not only tight monetary policy but also broader economic stability.

What This Means for Business

There are no universal strategies, but several practical conclusions emerge for companies working with Turkey or considering it in their strategies for 2025–2026.

- Treat 2026 as a year of testing stability, not as guaranteed recovery in investor sentiment.

- Distinguish between stabilization and growth. The current policy mix reduces depreciation and inflation but keeps growth moderate.

- Monitor the exchange rate trajectory as a key indicator. The reduction in depreciation from 86% to 18% is highly relevant for contracts, procurement, import costs, and investment calculations.

- Assess the external environment carefully. If monetary easing in developed economies materializes, financing conditions may improve. However, slower global growth could limit export demand.

- Do not overestimate the shift in trade routes. The potential exists but remains only partially realized, and political factors still play a major role.

For these reasons, 2026 may become a decisive year — revealing whether the current normalization remains a short episode or evolves into a sustainable trajectory that businesses can rely on.

Operational Efficiency in Treasury: Liquidity Centralisation and Readiness for 24/7

Why the shift to 24/7 and instant settlement breaks not technology first, but the operating model itself: where liquidity actually sits, who has the full picture, how value dates work — and what happens if the payment rails have to be stopped.

FX Risk in Volatile Markets: Building a Robust Risk Management Framework in Banks

Why, in periods of high FX volatility, selecting a hedging instrument is not enough—and how to build a structured FX-risk management system. Which metrics to use for daily monitoring, how to match instruments to specific risk types and liquidity constraints, and what management lessons can be drawn from hedging failures at major banks.