From ESG Reporting to Capital and Liquidity: What Changes for Banks

Why has ESG moved beyond disclosure and become a question of banks’ financial resilience? Where exactly will supervisors look at capital, liquidity, and funding — and what does this change for treasury?

How can banks turn ESG and climate targets into a manageable financial plan — with capital, liquidity, and clear actions under stress scenarios?

Mirko De Giovanni, Senior Advisor at IFC (World Bank Group), outlines an approach where ESG factors are not treated as a standalone agenda, but as drivers that reshape traditional banking risks, prudential regulatory requirements, and supervisory expectations.

In this logic, the core question is straightforward: a bank may publicly commit to targets for 2030 or 2050 — but is it clear how those targets will be financed, through funding, balance-sheet structure, and scenario analysis? And just as importantly: who inside the organisation is accountable, and how is this embedded in governance?

Why ESG Has Become a Financial Stability Issue

As long as ESG sits in a separate silo, it looks like a reputational topic. Once targets require funding and start altering the pricing of risk, it becomes a balance-sheet resilience issue. Three numbers quickly bring the discussion back to reality:

- USD 4.5 trillion per year — estimated by the IEA as the annual investment needed for the energy transition this decade.

- USD 1.7 trillion — the amount actually invested in 2024.

- 65% of residual emissions come from hard-to-abate sectors (cement, steel, heavy transport, oil & gas, and others).

This creates two gaps.

The first is a funding gap: the capital required exceeds what is currently flowing.

The second is an allocation gap: even the funds that are deployed often bypass precisely those sectors that will determine whether global warming can be kept within relatively safe limits.

This is where bank resilience comes into play. If a significant share of transition financing runs through banks, the challenge is how to channel capital faster and more precisely — without blowing off prudential safeguards in the form of capital and liquidity requirements or creating new balance-sheet risks.

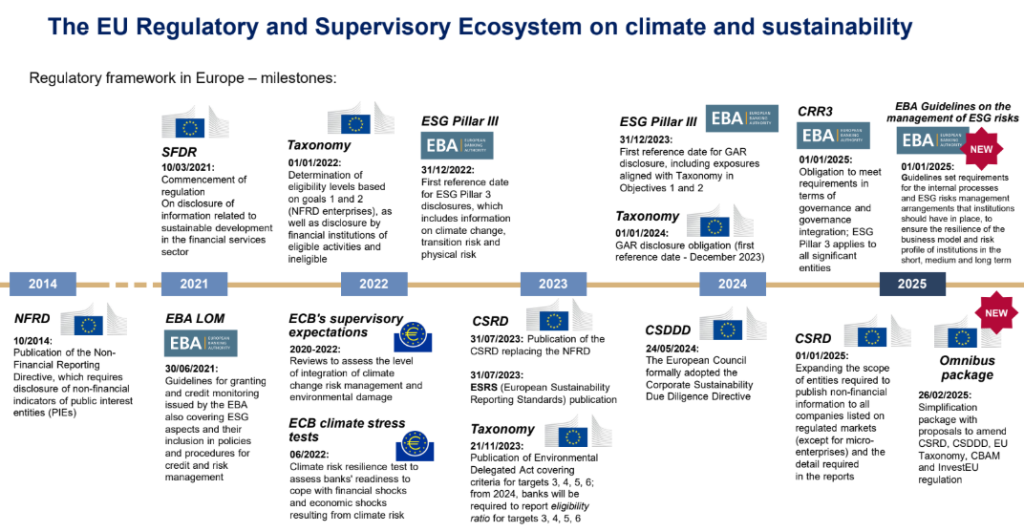

In the EU, ESG is already embedded in mandatory requirements governing disclosure, risk management, governance and resilience testing — from supervisory expectations and stress tests to frameworks such as the EU Taxonomy, SFDR, CSRD/ESRS, and the updated banking rules under CRR3 and CRD VI. Put simply, the rules of the game are changing: supervisors increasingly assess not ESG statements or standalone reports, but whether ESG risks are embedded in core banking processes. This directly affects the supervisory review (SREP) and may translate into additional Pillar 2 capital requirements, while the Pillar 1 framework awaits re-assessment.

EBA 2025: What Is Required and When

In January 2025, the European Banking Authority (EBA) issued guidelines on the management of ESG risks. For large banks, these become binding from 11 January 2026; for small and non-complex institutions (SNCIs), from 11 January 2027.

The guidelines define a baseline minimum: how banks must identify, measure, manage, and monitor ESG risks; what must be included in the CRD VI Article 76(2) transition plan; how impacts should be assessed qualitatively and quantitatively; and, in particular, how scenario analysis should be applied.

As a complement, in November 2025 the EBA also published ESG Scenario Analysis Guidelines, which set out expectations for institutions when adopting forward-looking approaches and incorporating the use of scenario analysis as part of their management framework to test their financial and business model resilience to the short- and long-term negative impacts of ESG factors. ESG Is Not a New Risk Category

ESG is not an additional risk that can be parked in a separate report. It consists of factors that transmit to and amplify traditional banking risks — credit, market, liquidity, operational, business model, concentration and others. The implication is clear: rather than building a parallel framework, banks must embed ESG factors into existing risk management processes, tools, methodologies and frameworks — risk appetite, ICAAP/ILAAP, ALM scenarios, internal controls, and management decisions.

The argument “we already do all this” does not hold. If ESG affects conventional risks, then banks already carry these exposures in their portfolios. The real question is whether they are visible in methodologies and governance — or remain blind spots.

Three Building Blocks of ESG Risk Management

1) Materiality

According to the EBA GLs, at least annually (every two years for SNCIs), banks must assess whether ESG risks are material and through which channels they affect traditional risks. The assessment must be both qualitative and quantitative — including impacts on financial, such as capital and liquidity, and profitability metrics — and embedded into ICAAP, and shall cover all relevant time-horizons (short, medium and long-term of at least 10 years). If the assessment points to ‘non-materiality’, institutions must carefully, transparently and comprehensively substantiate it.

Some key minimum requirements include: one adverse physical-risk scenario (for SNCIs), at least one portfolio-alignment (forward-looking) methodology employed, and an assessment of exposures to high-carbon sectors, similar to key exclusions under the EU BMR.

2) Measurement

Client-level analysis alone is insufficient. Banks need a combination of three lenses: counterparty/exposure, sector/portfolio, and scenarios. Assumptions (baseline, scenarios, scope) must be transparent, and data must allow segmentation by geography, sector, asset, or activity.

3) Management and Monitoring

ESG must be reflected in the risk appetite through concrete KRIs — ideally both back-ward and forward-looking — with a clear escalation process, audit trails, reporting lines and management actions when limits are breached. Common failures include insufficient granularity, unclear methodologies, hidden data gaps, and purely formal yet ineffective escalation.

What Supervisors See — and Why “Green” Logic Often Fails

Supervisory observations highlight a gap between acknowledging ESG risks and managing them.

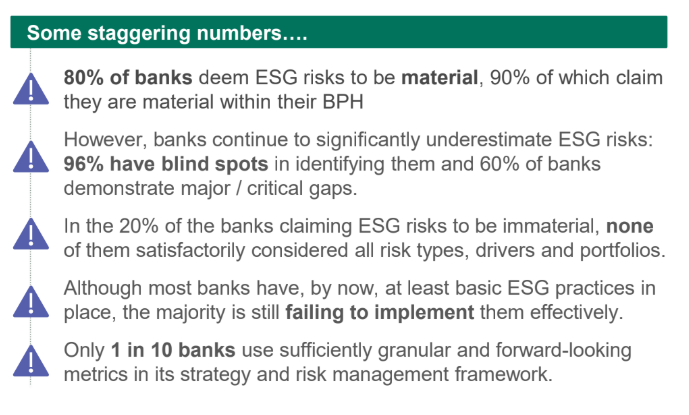

According to an assessment by the ECB, around 80% of banks consideredESG risks material, among which 90% classified them as material within the business-planning horizon. Yet 96% manifested blind spots in risk identification, 60% faced serious or critical gaps, and only one in ten used sufficiently granular and forward-looking metrics in strategy and risk management. Although there has been significant progress in recent years, supervisors still witness material gaps in ESG risk identification, measurement, management and monitoring in EU financial institutions, which has led to a stronger supervisory push around ESG risk management, culminating in the publication of the EBA Guidelines.

The takeaway is simple: supervisors no longer ask whether ESG exists on paper, but whether it works — whether it changes tools, risk profiles, and decisions. This also explains why “mainstream green finance” often delivers limited impact:

- funding targets individual projects rather than transforming entire business models;

- green labels certify use of proceeds, not the issuer’s transition trajectory;

- public commitments are often disconnected from governance, incentives, and CAPEX;

- markets favour quick wins over long-term transformation;

- accountability for missed targets has historically been reputational — and this is precisely what supervisory pressure is now changing.

Importantly, the critique of “green labelling” is not universal. In asset-backed products — for example, portfolios of green real estate — the link between instrument and underlying asset is typically much stronger than in general corporate financing.

Transition Plans and the Role of Treasury: From Targets to Funding

In the EU, transition plans are becoming a mandatory element of banking regulation. Under EBA Guidelines, which are enshrined in CRD VI (Art. 76(2), precisely) , this enters into force in 2026, in a push to foster alignment with and promote the EU targets of –55% emissions by 2030 and climate neutrality by 2050.

Such a plan must rest on three pillars:

- Resilience: the balance-sheet impact under adverse scenarios.

- Integration: whether targets and risks are embedded in strategy, risk appetite, ICAAP/ILAAP, capital, and funding.

- Consistency: alignment between the plan’s assumptions and public disclosures and reporting.

The quality check is straightforward: the plan must answer, with numbers, timelines, governance and funding, four questions — where are we going, how will we get there, how will we pay for it (investments and financial plan), and who is accountable.

This is why treasury and ALM move to centre stage. A bank may commit publicly to a trajectory, but without a credible funding, liquidity, and scenario framework, the “how do we pay for it” section becomes a formality. Supervisors assess coherence and realism, not declarations — with direct implications for SREP and potential Pillar 2 capital add-ons.

Treasury in Practice: Six Areas That Will Need Rethinking

Balance-sheet planning

Incorporate clients’ CAPEX plans to better forecast sectoral funding demand, maturities, and refinancing peaks — and reflect this in tenor structure, FTP, and liquidity buffers.

Liquidity

Embed ESG factors into ALM scenarios and liquidity stress tests: deposit outflows, drawdowns, HQLA revaluation. Define ex-ante management actions for each scenario.

HQLA and collateral

Review HQLA composition and collateral haircuts for ESG risk: stranded-asset risk, transition exposure, and the quality of issuers’ transition plans.

Funding

Assess how ESG affects access to, cost, and stability of funding; develop issuance programmes (green, social, sustainability-linked) and maintain a clear pool of eligible assets aligned with use-of-proceeds and taxonomy requirements.

Market risk

Update limits, hedging approaches, and monitoring: ESG factors can materially alter issuers’ sensitivity to regulatory and energy-price shocks.

Governance

Make ESG a standing ALCO agenda item: introduce clear (preferably forward-looking) KRIs, link treasury metrics to the transition plan, and ensure real escalation when thresholds are breached.

Treasury Metrics: What to Measure to Stay in Control

To prevent ESG from dissolving into generic statements, it must be tied to measurable indicators, some of which, depending on the institutions’ exposure profile and business model, could be:

Funding and liquidity

- share of green/social/sustainable funding in total funding;

- share of HQLA aligned with ESG criteria;

- carbon-adjusted cost of funds;

- share of funding allocated to EU-taxonomy-aligned or transition-plan-aligned assets;

- number of ESG-focused investor engagements;

- financed Scope 3 emissions per unit of treasury funding.

Processes and governance

- treasury’s involvement in the transition-planning process;

- share of treasury policies updated for climate/transition risk;

- frequency of climate-related funding and liquidity stress tests;

- training hours for treasury staff on ESG and transition topics.

Key Takeaways

- Move ESG from a standalone topic into core banking and non-banking processes and methodologies. If ESG affects credit, market, liquidity, concentration, operational and business model risk, it must be visible in risk appetite, risk management, ALM scenarios, and capital and liquidity planning.

- What matters is impact, but do not forget documentation. Supervisors look for changes in decisions and risk profiles — and for clear substantiation of data, models, and management actions.

- Close the chain between targets, funding, and accountability. A credible transition plan is anchored in the financial plan, funding and liquidity strategy, metrics, and clear ownership.

In this agenda, the winners are not those who promise the loudest, but those who can translate targets into actionable roadmaps, strategies, liquidity and funding plans and metrics.

High Liquidity Is Not Always a Good Thing: How to Set the Right Targets

How do you define the “right” level of liquidity when a high ratio alone does not guarantee optimality? We explore a practical framework: separating liquidity into a risk buffer and a managed strategic resource, building a ladder of target levels, and using FTP to keep liquidity within an effective operating corridor.

Non-Maturity Deposits Under Rate Stress: What to Look for in Data and Segmentation or Rethinking NMD modelling beyond averages

Why the “core” of non-maturity deposits cannot be estimated by inertia: sharp rate movements, the growing gap between historical models and current behaviour, and what banks must challenge in their assumptions.