Currency Volatility and Bank Margins: How to Measure the Effect and Calibrate FTP

In emerging economies, the exchange rate is more than just a macro indicator. It influences investor decisions, corporate and banking balance sheets, and ultimately financial performance. In Turkey, this effect is particularly visible: after 2018, currency dynamics became more sensitive to local shocks, and volatility spikes became more frequent.

Public discussions often feature conflicting narratives: “margins are compressing” or “banks benefit from turbulence.” Without measurement, however, these remain opinions. Melikşah Baykal, Senior Treasury Analyst at Hayat Finans (Turkey), explained how a simple analytical bridge can be built between econometric estimation and a practical treasury task: calibrating Funds Transfer Pricing (FTP).

Context: Why Turkey Is a Useful Case Study

Turkey provides an interesting analytical setting for two reasons.

First, the country hosts both conventional banks and participation banks. This allows a comparison of how the same external factor — currency volatility — affects margin dynamics across different banking models.

Second, the macro-financial environment changed significantly after 2018. Prior to that period, financial stability was higher and funding costs were relatively lower. After 2018, the economy experienced a series of local shocks, and the USD/TRY exchange rate became more vulnerable.

This is an important methodological point: combining “pre-2018” and “post-2018” periods in one estimation effectively averages two different regimes and may obscure the true effect of the current environment.

From Intuition to Measurable Margin Sensitivity

The key question is straightforward: how much does a bank’s margin change when FX volatility changes?

Once this sensitivity is estimated, it can be used as a reference in FTP — for example, as a basis for margin adjustments or risk premia when volatility increases.

However, estimating this correctly requires more than simply linking a volatility indicator to margins. Otherwise, FX volatility may inadvertently capture the influence of monetary policy, inflation, or global risk appetite.

Therefore, the analysis separates:

- domestic factors (policy rate, inflation),

- external conditions (global volatility / risk appetite),

- and FX volatility itself.

Data and Methodology: What Is Being Estimated

In this framework, bank margins are defined as follows:

- For conventional banks, the analysis uses net interest margin (NIM) based on data from the Central Bank of the Republic of Turkey (CBRT), available since 2002.

- For participation banks, data is available only from 2018 onward, so the analysis focuses on the 2018+ period and uses net financing margin.

FX volatility is measured using the USD/TRY exchange rate and estimated through a conditional volatility model (sGARCH), producing a time series of volatility estimates.

The model includes the following control variables:

- the CBRT policy rate (1-week repo),

- CPI inflation,

- the VIX index as a proxy for global volatility and risk appetite.

The logic is straightforward: without control variables, FX volatility may absorb the effects of other macroeconomic drivers, making the estimate less useful from a management perspective.

All independent variables enter the model with a lag. The assumption is that volatility in the previous month affects the margin in the current month. This also helps mitigate simultaneity issues, where margins and volatility could otherwise be determined at the same time.

What Comparisons Are Performed

Two sets of comparisons are conducted:

- For conventional banks — comparing the periods before and after 2018.

- For the 2018+ period — comparing conventional banks and participation banks.

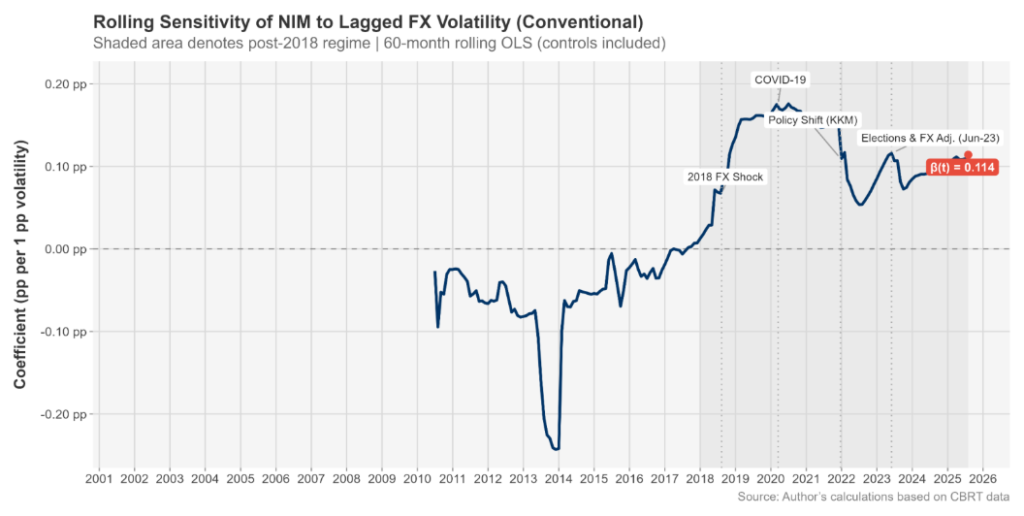

Results: What Changes After 2018

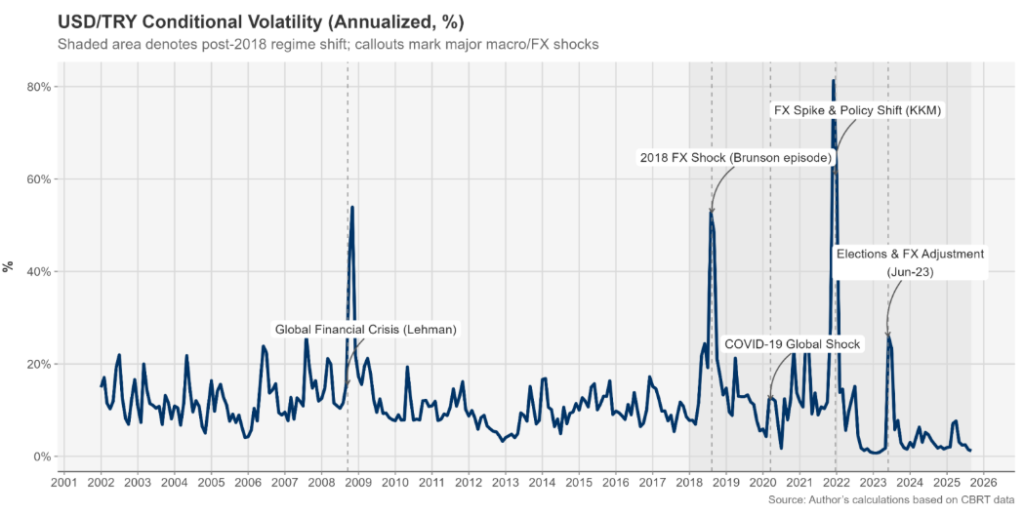

1. Volatility becomes more frequent and more locally driven

The conditional volatility time series shows that after 2018, spikes occur more frequently than under the previous regime. The key takeaway is not the chart itself but its interpretation: the environment shifted toward a regime where currency uncertainty became a persistent feature.

2. The relationship between volatility and margins depends on the regime

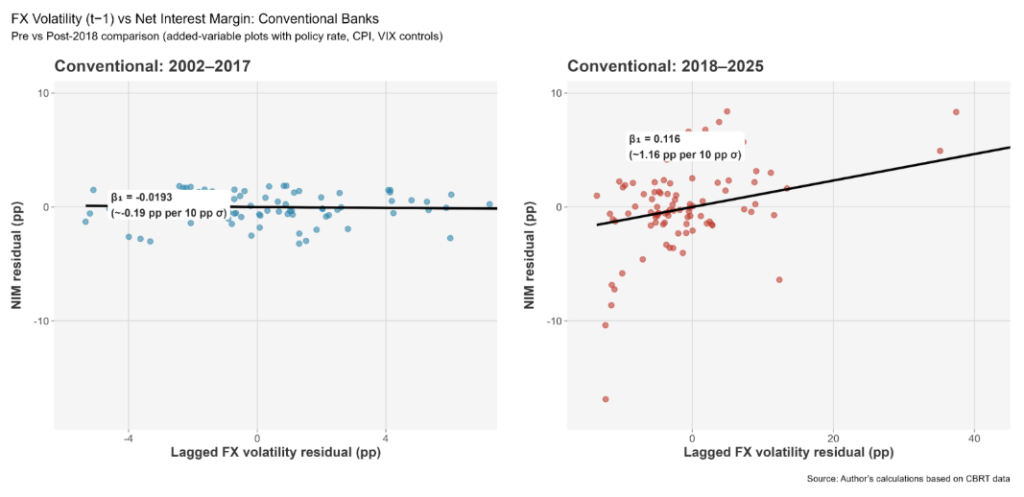

Looking at the entire historical period may produce an averaged result. However, this can be misleading because the system behaves differently before and after 2018.

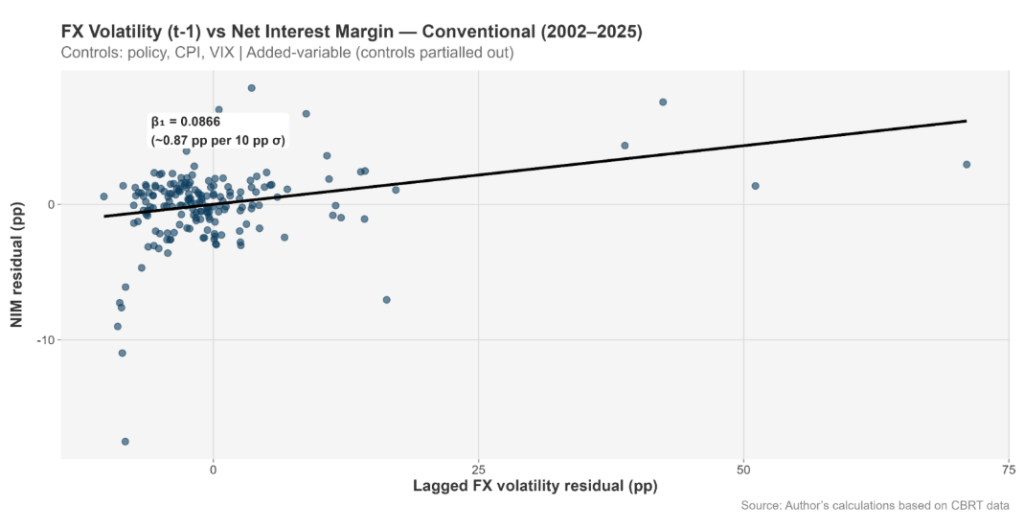

Before 2018, the relationship between FX volatility and NIM for conventional banks appears almost flat — volatility had a limited impact on margins.

After 2018, the relationship becomes clearly positive: increases in volatility are associated with higher margins.

This result should be interpreted carefully. A rising margin does not mean volatility is beneficial. Rather, it indicates that banks are repricing risk, and margins begin to include a risk-premium component.

3. Participation banks react more strongly than conventional banks

During the 2018+ period, both conventional banks and participation banks show a positive relationship between volatility and margins. However, the effect is stronger for participation banks.

According to the interpretation provided by Hayat Finans, this may reflect the income structure and product logic of participation banking — including profit-sharing mechanisms, regulatory frameworks, and specific adjustment channels compared with interest-based models — leading to a stronger margin response to volatility shocks.

4. The role of policy rates, inflation, and the VIX

Regression results also indicate that:

- the policy rate has a positive effect on margins,

- CPI inflation is statistically significant for participation banks, consistent with their revenue structure,

- the VIX index does not show a significant impact on margins.

This suggests that margin dynamics during the period studied are driven primarily by local factors rather than global shocks.

Why Rolling Estimates Matter

A static regression provides a single coefficient. In practice, however, the key question is different: how stable is this sensitivity over time?

To address this, a rolling regression approach is used with a 60-month moving window. The regression is recalculated each month while shifting the window forward.

The results show that after 2018 the estimated coefficients behave differently, confirming that the system experienced a structural regime shift rather than a temporary anomaly.

Practical Application: Using the Estimates in FTP

Once the sensitivity of margins to volatility is estimated, banks can translate this into FTP calibration.

The mechanics are straightforward:

- convert the estimated coefficient into basis points,

- define scenarios (for example, a given increase in volatility),

- calculate pass-through options (100%, 50%, 25%).

This example represents a minimal working framework. Each bank should calibrate the model based on its own balance sheet and risk profile. Nevertheless, the principle provides an important advantage: FTP decisions become structured and comparable over time, rather than purely reactive.

Limitations and Possible Extensions

The approach described above is intentionally simple, but it can be further developed.

Possible extensions include:

- using more advanced identification methods such as instrumental variables or local projections,

- testing alternative volatility models (for example EGARCH),

- moving from aggregated data to product- or portfolio-level analysis, if available,

- refining the inflation measure (for instance, using core inflation instead of CPI),

- incorporating qualitative or structural variables that better capture the specifics of an individual bank.

The value of the exercise is not in celebrating volatility. Its value lies in measuring its impact and translating that estimate into actionable FTP parameters, turning discussions about shocks and risks into manageable and quantifiable decisions.

FX Risk in Volatile Markets: Building a Robust Risk Management Framework in Banks

Why, in periods of high FX volatility, selecting a hedging instrument is not enough—and how to build a structured FX-risk management system. Which metrics to use for daily monitoring, how to match instruments to specific risk types and liquidity constraints, and what management lessons can be drawn from hedging failures at major banks.