FX Risk in Volatile Markets: Building a Robust Risk Management Framework in Banks

Currency volatility is dangerous because an open FX position can suddenly deteriorate a bank’s risk profile. This can quickly lead to pressure on limits, liquidity management, and portfolio resilience under stress scenarios. Without a transparent system of limits, stop mechanisms, and regular scenario testing, hedging itself can become a new source of risk.

Alp Özkan, Deputy Head of Market Risk at QNB Türkiye, shared the practical logic of moving step by step from identifying FX exposure to selecting hedging instruments and establishing daily risk control—especially when markets become nervous and liquidity is constrained.

Building an FX Risk Management Framework

At QNB Türkiye, specialists follow a simple sequence:

- Make the FX exposure visible (including balance sheet positions and derivatives).

- Measure risk using metrics and stress scenarios.

- Select instruments according to the type of risk and market constraints.

- Embed the process in governance—limits, stop-loss rules, monitoring, and regular model and policy reviews.

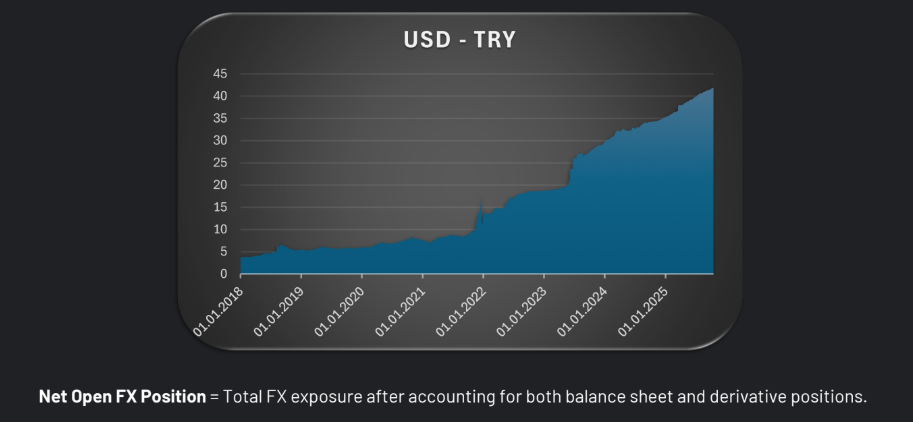

This sequence matters because FX risk often arises not only from balance-sheet positions but also from derivative transactions that contain a currency component. Therefore, the starting point is the Net Open FX Position—the aggregate open currency exposure that combines balance-sheet items with derivative positions.

Once this exposure is clearly defined, risk can be managed proactively rather than reactively, within predefined and agreed risk limits.

Distinguishing Types of FX Risk

The next step is to classify FX risk by its nature and time horizon. This prevents different risk types from being bundled into a single universal hedge.

Transaction risk

Short-term risk related to cash flows. Typically hedged using forwards, FX swaps, or cross-currency swaps.

Translation risk

Arises when operations take place in one country while part of the corporate structure or reporting is linked to another jurisdiction. Currency volatility may therefore affect balance-sheet values and financial reporting.

Economic risk

Strategic risk related to how currency movements influence competitiveness and long-term business value. This is typically addressed at the board level. Poor strategic decisions can leave a company vulnerable in international markets.

In practice, the sequence is straightforward:

first define which risk is being managed and over what horizon, then determine the limits and controls, and only then select the hedging instruments that fit within this framework.

Measuring FX Risk: Metrics and Ongoing Monitoring

Once exposure is defined, the next step is to make the risk measurable and comparable with established limits. At QNB Türkiye, a combination of metrics and procedures supports daily risk management.

Value-at-Risk (VaR 99%)

Estimates potential daily loss under normal market conditions.

Expected Shortfall (ES 97.5%)

Measures tail risk beyond VaR and is more sensitive to stress regimes.

Greek sensitivities (Delta, Vega, Gamma)

Monitored through risk dashboards, particularly important when the portfolio contains options.

Stop-loss framework

Daily and cumulative triggers designed to limit potential losses.

Stress testing and scenario analysis

Assess the portfolio’s resilience to extreme FX and liquidity shocks.

Reporting cadence

Daily dashboards, weekly stress reports, and monthly risk committee reviews.

Importantly, risk measurement does not rely on a single model. Parametric, historical simulation, and Monte Carlo approaches are used in parallel for comparison and validation.

The Role of Greeks

Greeks provide a concise language for understanding how the portfolio reacts to market changes, particularly for options, where behaviour can be nonlinear.

Delta measures how much a position’s value changes when the underlying price moves slightly.

Vega shows sensitivity to volatility changes. For options, volatility shifts can significantly affect pricing even without large FX movements.

Gamma measures how rapidly Delta itself changes as the underlying price moves. This captures the nonlinear nature of option risk—portfolio sensitivity can accelerate as markets move.

Choosing Instruments Based on Risk, Horizon, and Liquidity

Instrument selection depends on three factors: risk type, time horizon, and market liquidity or accessibility.

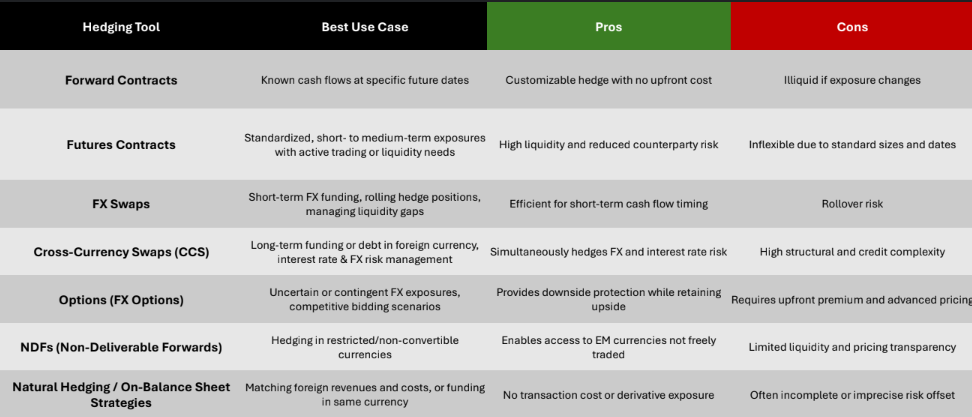

Forwards

Used when cash flows and settlement dates are known. They offer flexibility and no upfront cost. The drawback is reduced flexibility if exposure changes.

Futures

Suitable for standardized exposures and markets where liquidity and lower counterparty risk are priorities. However, contract sizes and maturities are fixed.

FX Swaps

Often used for short-term FX funding, rolling hedges, and liquidity gap management. The key risk is rollover risk.

Cross-Currency Swaps (CCS)

Appropriate for long-term foreign-currency funding and simultaneous management of interest-rate and FX risk. These structures are more complex and involve greater credit exposure.

Options

Useful for uncertain or contingent exposures, such as competitive tenders. They provide downside protection while preserving upside potential but require upfront premiums and sophisticated valuation and risk control.

Non-Deliverable Forwards (NDF)

Commonly used for restricted or non-convertible currencies where direct hedging markets are limited. Liquidity and pricing transparency can be challenges.

Natural Hedging / Balance-Sheet Strategies

Matching FX revenues with FX costs or funding in the same currency. This avoids derivative transaction costs but often results in imperfect hedges.

When markets tighten, expanding the set of workable solutions becomes critical. Flexible strategies—partial hedges, rolling hedges, NDFs, and balance-sheet buffers—help maintain risk control.

Structuring the FX Hedging Process in a Bank

FX risk management is embedded as a unified practice:

- standardized FX policies and governance across business units

- clearly defined risk appetite and escalation framework

- integrated monitoring and reporting

- daily management using VaR, ES, and Greeks

- layered hedging and counterparty diversification

- regular policy and model reviews

- alignment between front-office strategy and risk governance

Without a unified framework, FX risk tends to drift across products and departments, and decisions become reactive rather than structured.

Managing FX Risk in a Geopolitically Unstable Environment

Sanctions, capital controls, and convertibility restrictions require additional preparation. Key responses include:

- early stress testing of geopolitical scenarios

- FX liquidity buffers in USD/EUR and access to global credit lines

- flexible hedging structures such as options or rolling hedges

- shorter tenors and higher tactical flexibility

- regional and counterparty diversification

- crisis playbooks and ongoing dialogue with regulators

In practice, major losses often occur not because instruments are unavailable, but because of scale, complexity, or a disconnect between individual trades and overall risk governance.

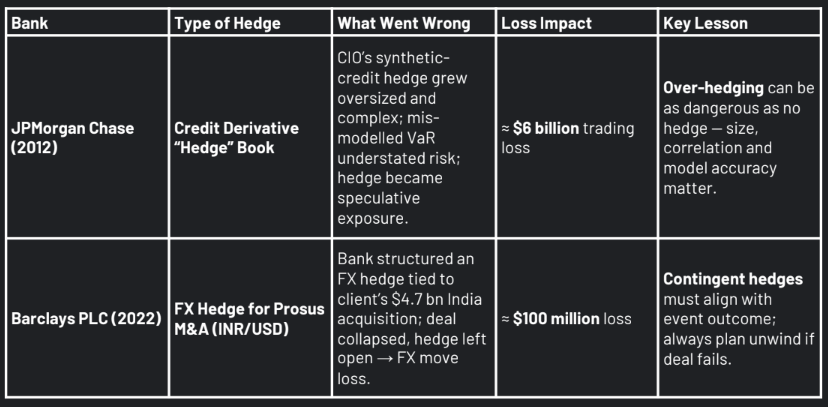

Lessons from Hedging Failures

JPMorgan (2012)

A credit hedging portfolio became overly large and complex. A flawed VaR model underestimated risk, turning the hedge into a speculative exposure. The result was approximately $6 billion in trading losses.

Key lesson: over-hedging can be as dangerous as not hedging at all.

Barclays (2022)

An FX hedge tied to a potential INR/USD M&A transaction remained open after the deal collapsed, resulting in roughly $100 million in losses.

Key lesson: contingent hedges must be aligned with the outcome of the underlying event, and unwind strategies should be planned in advance.

Practical Takeaways

A manageable FX hedging framework requires:

- a unified definition of exposure (Net Open FX Position) and transparent limits

- a consistent set of metrics and procedures (VaR, ES, Greeks, stop-loss rules, stress testing) supported by regular reporting

- selecting instruments based on risk type, time horizon, and liquidity constraints rather than relying on a single universal hedge

- readiness for market restrictions through liquidity buffers, flexible strategies, and counterparty diversification

- strong governance discipline: coordination between front office and risk management, with regular policy updates

And the core principle that underpins the entire system:

“Hedge when you can—not when you are forced to.”

Turkey 2026: Economic Stability, the Lira and Key Risks for Business

For companies planning production, sourcing, exports, or investment in Turkey in 2025–2026, one question dominates: is the country entering a period of sustainable stabilization, or is the current calm merely temporary? According to Şevin Ekinci, 2026 may provide the answer. She explains which domestic indicators will determine whether the normalization holds, how the global economic environment is shifting, and why two specific risks could quickly reverse the trajectory.

Currency Volatility and Bank Margins: How to Measure the Effect and Calibrate FTP

Exchange-rate volatility in Turkey after 2018 has become not an episodic shock but a persistent factor linked to the dynamics of banking margins. Once this relationship is measured and the influence of local and global factors is separated, it becomes a practical tool. The estimated sensitivity of margins to volatility can then be used as a reference parameter for Funds Transfer Pricing (FTP).